How to Check Your Credit Score Without Hurting It?

Credit scores play a crucial role in our financial lives. Whether you're applying for a loan, a mortgage, or even a new job, your credit score can impact your opportunities. But many people hesitate to check their credit scores, fearing that doing so could lower them. The good news? Checking your credit score doesn’t have to hurt it. In this guide, we’ll explore how to safely check your credit score, debunk some common myths, and offer tips to keep your credit score healthy.

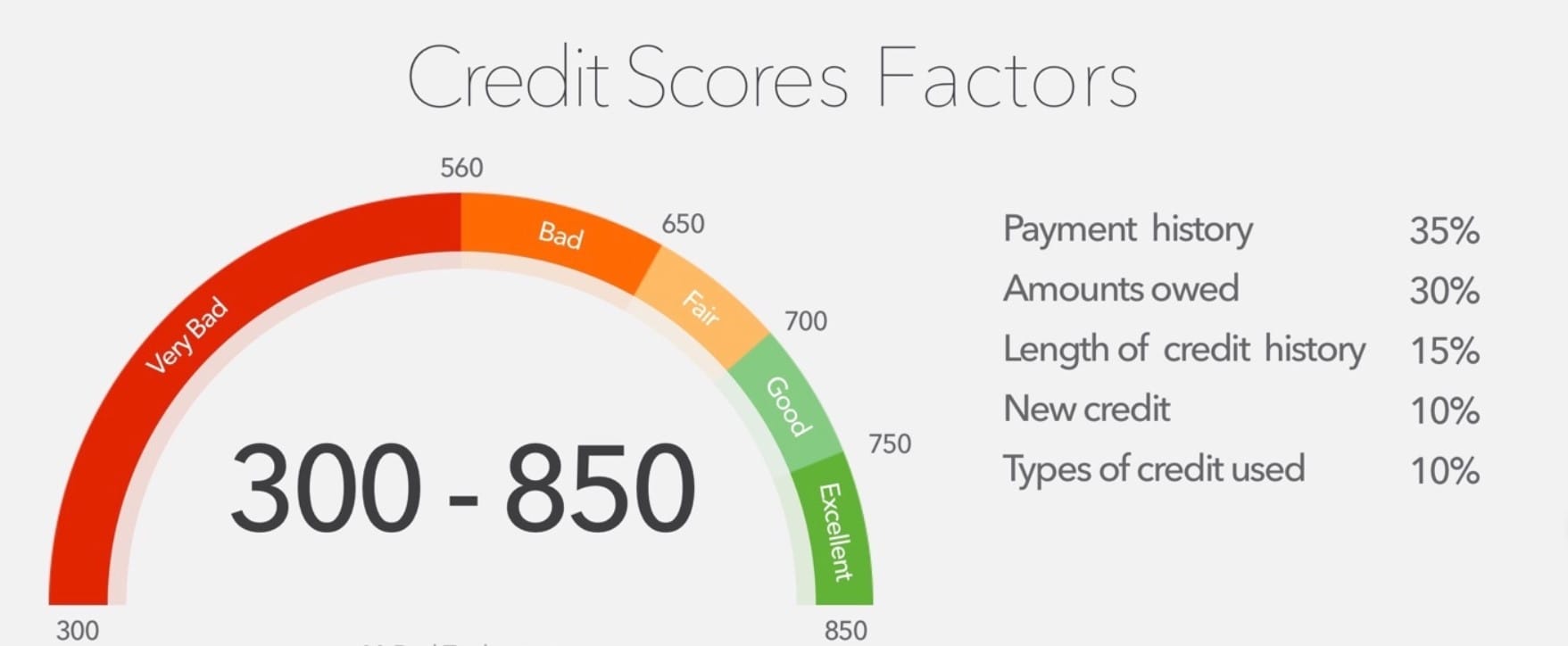

Understanding Credit Scores

What is a Credit Score?

A credit score is a numerical representation of your creditworthiness. Lenders, landlords, and even employers use this score to assess how likely you are to repay debts or fulfill financial obligations. The score typically ranges from 300 to 850, with higher scores indicating better creditworthiness.

How is a Credit Score Calculated?

Your credit score is calculated based on several factors, including:

- Payment History: Your track record of on-time payments.

- Credit Utilization: The ratio of your credit card balances to your credit limits.

- Length of Credit History: How long you’ve had credit accounts.

- New Credit: Recent credit applications could indicate financial stress.

- Credit Mix: A variety of credit accounts, such as credit cards, installment loans, and mortgages.

Why You Should Check Your Credit Score Regularly

Monitoring Financial Health

Just like you regularly check your bank account balance, monitoring your credit score helps you keep track of your financial health. Regular checks can alert you to any issues, such as identity theft or errors in your credit report, allowing you to address them promptly.

Preparing for Major Financial Decisions

If you’re planning to make a significant financial move, such as buying a home or applying for a loan, knowing your credit score in advance gives you time to improve it if necessary. A higher credit score can lead to better interest rates and loan terms.

Identifying Errors and Fraud

Mistakes on your credit report can drag down your score. Regularly checking your credit score helps you identify and dispute errors or fraudulent activities that could harm your credit.

Will Checking Your Credit Score Lower It?

Understanding Hard Inquiries vs. Soft Inquiries

One of the most common concerns people have is that checking their credit score will lower it. However, it’s essential to distinguish between two types of credit inquiries: hard inquiries and soft inquiries.

- Hard Inquiries: These occur when a lender checks your credit report to make a lending decision. Hard inquiries can slightly lower your credit score, especially if you have several in a short period.

- Soft Inquiries: These occur when you or a third party checks your credit for informational purposes, not for lending decisions. Checking your own credit score is considered a soft inquiry and does not affect your score.

The Myth of Self-Inquiries Hurting Your Credit Score

There’s a widespread myth that checking your own credit score can damage it. In reality, this is not true. Soft inquiries, including those you initiate, do not impact your score. You can check your credit score as often as you like without fear of it dropping.

How to Check Your Credit Score Without Hurting It

Use Free Credit Monitoring Services

Several free credit monitoring services allow you to check your credit score regularly without affecting it. These services often provide additional tools, such as credit score simulators, which can help you understand how different financial decisions might impact your score.

Popular free credit monitoring services include:

- Credit Karma

- Credit Sesame

- Experian Free Credit Report

Check Your Score Through Your Bank or Credit Card Issuer

Many banks and credit card issuers offer free access to your credit score as a perk of being a customer. These scores are typically updated monthly and do not require a hard inquiry.

Get Your Annual Free Credit Report

By law, you’re entitled to one free credit report per year from each of the three major credit bureaus: Equifax, Experian, and TransUnion. While these reports don’t always include your credit score, they do provide detailed information about your credit history, which can help you understand the factors influencing your score.

You can request your free credit report at AnnualCreditReport.com.

Factors That Can Affect Your Credit Score

Late Payments

Late or missed payments can have a significant negative impact on your credit score. It’s essential to pay all your bills on time to maintain a healthy credit score.

High Credit Utilization

Your credit utilization ratio, which is the percentage of your total available credit that you're using, plays a crucial role in your credit score. Aim to keep your credit utilization below 30% to avoid negatively impacting your score.

Multiple Credit Applications

Each time you apply for credit, a hard inquiry is added to your credit report. Multiple hard inquiries in a short period can lower your score, so it’s best to limit credit applications.

Length of Credit History

The longer your credit history, the better. If you’re new to credit, your score may be lower simply because there’s less data to assess your creditworthiness.

Credit Mix

Having a variety of credit accounts, such as credit cards, auto loans, and mortgages, can positively impact your score. However, this is a less significant factor compared to payment history and credit utilization.

Tips for Maintaining a Healthy Credit Score

Pay Your Bills on Time

Your payment history is the most significant factor in your credit score. Setting up automatic payments or reminders can help ensure you never miss a due date.

Keep Credit Card Balances Low

High credit card balances can hurt your credit utilization ratio. Try to pay off your balances in full each month or keep them as low as possible.

Limit New Credit Applications

Only apply for new credit when necessary. Each application results in a hard inquiry, which can temporarily lower your score.

Review Your Credit Report Regularly

Checking your credit report for errors or signs of fraud can help you catch issues early and prevent damage to your score.

Consider Keeping Older Accounts Open

Closing older credit accounts can shorten your credit history and reduce your available credit, which might negatively impact your score. Unless there’s a good reason to close an account, it’s often better to keep it open.

Common Myths About Credit Scores

Myth 1: Checking Your Credit Score Hurts It

As we’ve discussed, checking your credit score through a soft inquiry doesn’t hurt your score. This myth often leads people to avoid monitoring their credit, which can be detrimental in the long run.

Myth 2: Closing Credit Cards Improves Your Score

Many people believe that closing unused credit cards will improve their credit scores. In reality, closing a card can reduce your available credit and shorten your credit history, both of which can lower your score.

Myth 3: You Only Have One Credit Score

You actually have multiple credit scores, depending on which credit bureau’s data is used and the scoring model applied. The three major credit bureaus—Equifax, Experian, and TransUnion—may have slightly different information, leading to different scores.

Myth 4: Paying Off Debt Always Increases Your Score

While paying off debt is generally good for your finances, it doesn’t always result in an immediate boost to your credit score. If you pay off an installment loan, for example, the closed account might reduce the variety in your credit mix, which could slightly lower your score.

Myth 5: Using a Credit Counselor Hurts Your Score

Working with a credit counselor to manage debt won’t hurt your credit score. It can help you improve your score over time by creating a plan to pay off debt and avoid missed payments.

Using Credit Score Simulators

How Credit Score Simulators Work

Credit score simulators are tools that allow you to see how different financial decisions might impact your credit score. For example, you can simulate the effect of paying off a credit card balance, opening a new account, or missing a payment.

Benefits of Using a Credit Score Simulator

These tools can be incredibly useful for planning your financial strategy. By understanding the potential impact of your actions, you can make informed decisions that help you maintain or improve your credit score.

Where to Find Credit Score Simulators

Many credit monitoring services, including Credit Karma and Credit Sesame, offer credit score simulators as part of their free tools. Some banks and credit card issuers also provide these simulators to their customers.

What to Do if Your Credit Score Drops

Identify the Cause

If you notice a drop in your credit score, the first step is to identify the cause. Review your credit report for any negative items, such as late payments, high balances, or new hard inquiries.

Dispute Errors

If the drop is due to an error on your credit report, you can dispute it with the credit bureau. Errors could include incorrect account information, fraudulent accounts, or outdated data.

Focus on Rebuilding

If the drop is due to legitimate factors, such as missed payments or high credit utilization, focus on rebuilding your score. This might involve paying down debt, making on-time payments, and avoiding new credit applications.

How Often Should You Check Your Credit Score?

Monthly Monitoring

Checking your credit score monthly can help you stay on top of any changes and catch issues early. This is especially useful if you’re actively working to improve your credit score or are planning a significant financial decision.

Quarterly Checks

If your credit is stable, quarterly checks might be sufficient. This allows you to monitor your credit over time without becoming too focused on minor fluctuations.

Before Major Financial Decisions

Always check your credit score before applying for a loan, mortgage, or other significant financial product. This ensures you’re aware of your credit status and can make any necessary improvements beforehand.

Protecting Your Credit Score from Fraud

Monitor for Unusual Activity

Regularly checking your credit report and score can help you catch signs of identity theft or fraud early. Look for unfamiliar accounts, hard inquiries you didn’t initiate, and significant drops in your score.

Use Fraud Alerts

If you suspect your information has been compromised, you can place a fraud alert on your credit report. This alert notifies potential creditors to take extra steps to verify your identity before opening new accounts.

Consider Credit Freezing

A credit freeze is a more drastic step that prevents anyone, including yourself, from opening new credit accounts in your name. It’s a good option if you’re not planning to apply for credit soon and want to protect yourself from identity theft.

FAQs

How can I check my credit score without it affecting my score?

You can check your credit score without affecting it by using free credit monitoring services, accessing it through your bank or credit card issuer, or requesting your annual free credit report. These methods involve soft inquiries, which do not impact your score.

How often should I check my credit score?

It’s a good idea to check your credit score monthly, especially if you’re working to improve it or planning a major financial decision. However, if your credit is stable, checking it quarterly might be sufficient.

What should I do if I find an error on my credit report?

If you find an error on your credit report, you should dispute it with the credit bureau that reported the error. Provide any supporting documentation and be prepared to follow up if necessary.

Does using a credit score simulator affect my score?

No, using a credit score simulator does not affect your credit score. These tools are designed to help you understand how different actions might impact your score without actually making those changes.

Is it better to keep old credit accounts open?

In many cases, it’s better to keep old credit accounts open, as closing them can shorten your credit history and reduce your available credit. However, if the account has high fees or poses a risk of overspending, closing it might be the better option.

Can paying off a loan lower my credit score?

Paying off a loan can sometimes result in a slight drop in your credit score, especially if it reduces your credit mix or shortens your credit history. However, the overall impact is usually minor, and the long-term benefits of being debt-free outweigh the temporary score decrease.

Conclusion

Checking your credit score is an essential part of managing your financial health, and it doesn't have to hurt your score. By understanding the difference between hard and soft inquiries, using free monitoring services, and regularly reviewing your credit report, you can stay on top of your credit without fear of damaging it. Remember, maintaining a healthy credit score requires ongoing attention and responsible financial habits. By paying your bills on time, keeping your credit utilization low, and monitoring your credit, you can ensure that your credit score remains strong, empowering you to achieve your financial goals.