Best Jewelry Store Credit Cards in 2026

Shopping for an engagement ring or diamond necklace? We break down the best jewelry store credit cards — and reveal the deferred interest trap most shoppers walk right into.

You're standing at the jewelry counter. The ring is perfect. The salesperson smiles and says, "Would you like to open a store credit card and get 12 months with no interest?"

It sounds like a no-brainer. But that offer comes with fine print that catches thousands of shoppers every year — and it's called deferred interest.

In this guide, we cover the best jewelry store credit cards available in 2026, explain exactly how each one works, and tell you honestly when a store card makes sense versus when you're better off pulling out a regular rewards card.

What Is a Jewelry Store Credit Card?

A jewelry store credit card is a private-label store card issued by a bank (usually Comenity or Synchrony) that can only be used at a specific jewelry retailer. These cards are almost always pitched at the point of sale with a promotional financing offer — typically 0% interest for 6 to 24 months.

Unlike general-purpose credit cards (Visa, Mastercard), you can't use a jewelry store card anywhere else. Their primary value is in financing a large purchase at a single retailer without immediate interest charges.

Most major jewelry chains in the US offer one:

- Helzberg Diamonds → Helzberg Credit Card (issued by Comenity Bank)

- Kay Jewelers → Kay Credit Card (issued by Comenity Bank)

- Zales → Zales Credit Card (issued by Comenity Bank)

- Jared → Jared Credit Card (issued by Comenity Bank)

- Blue Nile → Blue Nile Credit Card

- Riddle's Jewelry → Riddle's Jewelry Credit Card

- Crown Jewelers → Crown Jewelers Store Card (no credit check required)

- REEDS Jewelers → REEDS Credit Card (issued by Synchrony)

- Shane Company → Shane Company Credit Card (issued by Wells Fargo)

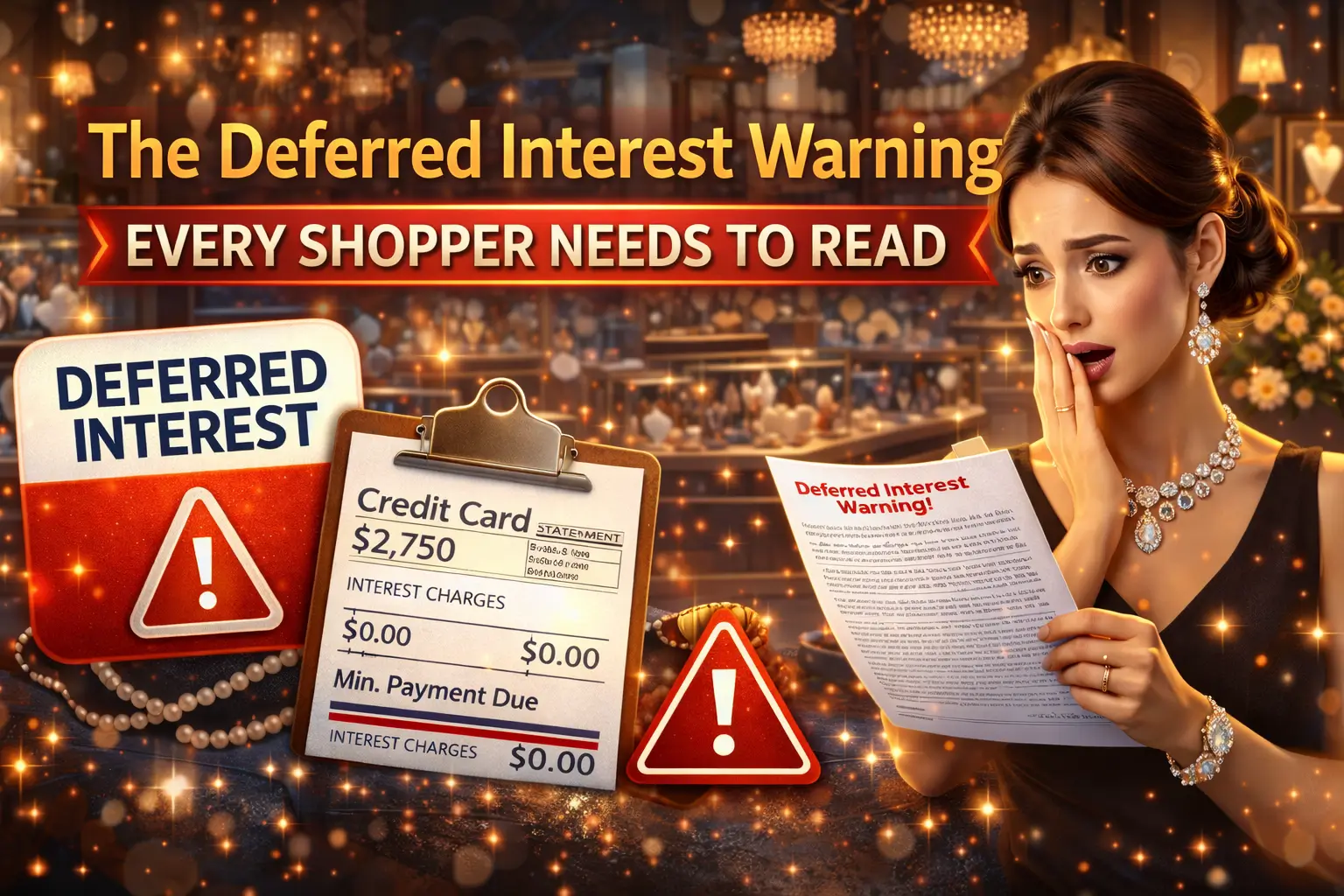

The Deferred Interest Warning Every Shopper Needs to Read

⚠️ STOP before you apply. Almost every jewelry store credit card uses deferred interest — not true 0% APR. This is the single biggest trap in jewelry financing.

Here's the difference:

| Feature | True 0% APR (regular card) | Deferred Interest (store card) |

|---|---|---|

| Interest during promo period | None charged | Calculated behind the scenes |

| If you pay off in time | Nothing owed | Nothing owed |

| If you miss even $1 | Still fine | All accrued interest hits your account retroactively |

| Interest charged from | End of promo period | Original purchase date |

Example: You finance a $2,000 engagement ring for 12 months with "no interest." You pay $1,950 of it. On day one of month 13, the store charges you interest calculated on $2,000 going all the way back to your purchase date — at the card's purchase APR, which is often 30–36%.

That "free" financing could suddenly cost you an extra $400–$600 in retroactive interest charges.

The only safe way to use a jewelry store card with deferred interest: pay the balance in full before the promotional period ends, and make sure to pay it — not just "on time" — but completely to zero.

Best Jewelry Store Credit Cards in 2026

1. Helzberg Diamonds Credit Card

Best for: Helzberg shoppers who need 6–24 months to pay off a large purchase

Issued by: Comenity Bank

Annual fee: $0

Credit required: Fair (640+)

Regular APR: 35.99% (as of March 2026)

Promotional financing options:

- 6 months no interest on purchases of $299+

- 12 months no interest on purchases of $999+

- 18–24 months no interest on select larger purchases

- 36-month equal-payment plan at reduced APRs (starting as low as 2.99%)

- 60-month plan at 9.99% APR for qualifying purchases of $2,999+

Bonus perks:

- $100 welcome bonus after first purchase (offer varies — confirm at time of application)

- Up to $50 off a purchase of $149.99+ as a birthday gift in year one

- Up to $75 holiday discount for cardholders

The catch: All "no interest" plans on the Helzberg card use deferred interest, not true 0% APR. The regular APR of 35.99% kicks in retroactively from the purchase date if you carry even $1 past the promotional deadline. The $2.99/month paper statement fee adds up if you don't enroll in paperless billing.

Our verdict: Among jewelry store cards, the Helzberg card offers one of the more flexible promotional ladders. The 36- and 60-month equal-payment plans with fixed low APRs are genuinely useful for very large purchases where you know you need extended time. If you're a Helzberg customer and your credit score is 640–699 (making you ineligible for premium travel or cash-back cards), this card is worth considering — with eyes open about deferred interest.

2. Kay Jewelers Credit Card

Best for: Kay shoppers with fair credit; those buying with a lower minimum spend

Issued by: Comenity Bank

Annual fee: $0

Credit required: Fair (640+)

Minimum purchase to use financing: $500

Regular APR: 17.99%–24.99% (varies by creditworthiness)

Promotional financing: 0% promotional period on qualifying purchases (deferred interest applies)

Kay is owned by Signet Jewelers, which also owns Zales and Jared — all three share a similar card structure. The Kay card's APR is notably more reasonable than Helzberg's 35.99%, with a range of 17.99%–24.99% depending on your credit profile. That still hurts if you trigger deferred interest, but the damage is less catastrophic.

Our verdict: A reasonable option for Kay loyalists with fair credit. The lower regular APR gives you a small safety net if the deferred interest trap is triggered. Pre-approval is not available online, so you'll need to apply in-store and accept a hard credit inquiry.

3. Zales Credit Card

Best for: Zales shoppers; same Signet family as Kay

Issued by: Comenity Bank

Annual fee: $0

Credit required: Fair (640+)

Zales operates under the same Signet Jewelers umbrella as Kay and Jared. The credit card structure is functionally similar: Comenity-issued, promotional financing with deferred interest, $0 annual fee. If you shop at Zales and your credit score limits your options, this card opens the door to promotional financing you might not get elsewhere.

Our verdict: Nearly identical to the Kay card in terms of structure and risk profile. Choose based on which store you prefer to shop at.

4. Jared Credit Card

Best for: High-value purchases with structured equal-payment financing

Issued by: Comenity Bank

Annual fee: $0

Credit required: Fair (640+)

Jared (also a Signet company) offers its Gold Card with a more structured financing approach. One common plan requires a minimum $1,000 purchase with a 20% down payment, with the balance financed over 12 months interest-free. For purchases over $5,000, a 20% down payment with 18-month financing is available.

The down payment requirement separates Jared slightly from its siblings — it reduces the total financed amount and can reduce your deferred interest exposure if you don't pay the full balance in time.

Our verdict: The down payment structure is a hidden positive — it forces discipline. If you're buying a high-ticket item at Jared, the structured equal-payment plans are worth understanding before you go in.

5. Blue Nile Credit Card

Best for: Online diamond and engagement ring shoppers

Annual fee: $0

Credit required: Fair (640+)

Promotional financing: 0% intro APR offers (deferred interest applies)

Blue Nile is the largest online-only diamond retailer in the US. Their credit card follows the standard store-card model: promotional 0% financing (with deferred interest), $0 annual fee, fair credit required. The card makes sense exclusively if you're buying from Blue Nile — its 0% period is genuinely useful for financing a large engagement ring over several months.

Our verdict: Fine for Blue Nile shoppers. Like all jewelry store cards, best used only if you're confident you can clear the full balance before the promotional period ends.

6. Riddle's Jewelry Credit Card

Best for: Shoppers in the Midwest looking for accessible fair-credit financing

Annual fee: $0

Credit required: Fair (640+)

Promotional financing: 0% intro APR (deferred interest)

Riddle's is a regional jewelry chain, and its card offers the same core proposition as the larger national brands — promotional 0% financing with deferred interest, $0 annual fee. One of the more accessible options if you're shopping at a Riddle's location.

7. Crown Jewelers Store Card

Best for: Shoppers with bad credit or no credit who need financing

Annual fee: $0

Credit check: Not required

Crown Jewelers stands out in this category for one important reason: no credit check required. This makes it the most accessible jewelry store card for people with damaged credit or no credit history. In a category where nearly every other card requires at least fair credit (640+), Crown Jewelers fills a genuine gap.

The trade-off is higher interest rates and limited store selection (Crown Jewelers is an online retailer). But if you need jewelry financing and your credit score is a barrier elsewhere, this is worth knowing about.

Best Regular Credit Cards for Jewelry Purchases

Here's the inconvenient truth most jewelry salespeople won't tell you: for shoppers with a credit score of 660 or higher, a general-purpose credit card is almost always a better deal.

Here are the top picks for buying jewelry with a regular credit card:

Chase Freedom Unlimited®

- Rewards: 1.5%–5% cash back on all purchases (1.5% on jewelry unless it falls in a bonus category)

- 0% Intro APR: 15 months on purchases (true 0% — no deferred interest)

- Annual fee: $0

- Why it wins: No deferred interest. The 15-month 0% window gives you ample time to pay off an engagement ring or anniversary gift. Plus you earn cash back on the purchase.

Bank of America® Customized Cash Rewards

- Rewards: Up to 6% cash back in your chosen category (online shopping qualifies)

- 0% Intro APR: 15 billing cycles

- Annual fee: $0

- Why it wins: If you buy jewelry online and select "online shopping" as your bonus category, you earn 6% back — a significant return on a $1,000+ purchase. Genuine 0% APR, no deferred interest trap.

Chase Sapphire Preferred®

- Rewards: 2x–5x points on various categories; 1x on jewelry

- Sign-up bonus: 60,000 points after spending $4,000 in first 3 months (worth ~$750 in travel)

- Annual fee: $95

- Why it wins: If you're buying an engagement ring over $4,000, you can hit the sign-up bonus threshold and walk away with enough points for flights on your honeymoon. Best for high-spend purchases where you can pay off immediately.

Wells Fargo Reflect® Card

- 0% Intro APR: Up to 21 months (longest on the market)

- Annual fee: $0

- Why it wins: The longest true 0% APR window available — nearly two years to pay off a purchase with zero interest, no deferred interest clause.

Jewelry Store Card vs Regular Credit Card: Which Should You Choose?

| Factor | Jewelry Store Card | Regular Credit Card |

|---|---|---|

| Usable at other stores | ❌ No | ✅ Yes |

| 0% APR offer | ✅ Yes (usually) | ✅ Yes (many offer it) |

| Deferred interest risk | ⚠️ High | ✅ None (true 0% APR) |

| Cash back / rewards | ❌ Minimal | ✅ Strong |

| Credit score required | Fair (640+) | Good–Excellent (660+) |

| Annual fee | ✅ Usually $0 | Usually $0–$95 |

| No credit check option | ✅ Crown Jewelers | ❌ No |

Choose a jewelry store card if:

- Your credit score is 640–659 and you can't qualify for a premium card

- You need a no-credit-check option (Crown Jewelers only)

- You're confident you will pay the full balance before the promo period ends

- The store-specific perks (birthday discount, welcome bonus) are meaningful to you

Choose a regular credit card if:

- Your credit score is 660 or higher

- You want to earn actual cash back or travel rewards on the purchase

- You're worried about accidentally triggering deferred interest (true 0% APR cards protect you)

- You want a card you can keep using beyond this purchase

Frequently Asked Questions (FAQs)

What credit score do I need for a jewelry store credit card?

Most jewelry store credit cards require a minimum credit score of around 640, which falls in the "fair credit" range. The Crown Jewelers store card is an exception — it doesn't require a credit check at all.

What is deferred interest and why does it matter?

Deferred interest means the credit card company is quietly calculating interest on your balance during the promotional period, but not charging it yet. If you pay off the full balance before the promo ends, you pay nothing. But if you carry even $1 past the deadline, all of that back-calculated interest gets applied retroactively from your original purchase date. On a $2,000 purchase at 35.99% APR, that can easily total $500–$700 in surprise charges.

Are there any jewelry store credit cards with no annual fee?

Yes — virtually all jewelry store credit cards have a $0 annual fee. The Helzberg card is a slight exception in that it charges $2.99/month if you receive paper statements; enrolling in paperless billing eliminates this fee.

Which is the easiest jewelry credit card to get?

The Crown Jewelers store card requires no credit check at all, making it the most accessible. Among traditional store cards, Helzberg, Kay, Zales, Jared, Blue Nile, and Riddle's are all roughly equivalent in requirements — they all require fair credit (640+). Your best bet is to apply for the card associated with whichever store you already plan to shop at.

Can I use a jewelry store credit card anywhere else?

No. Jewelry store credit cards are private-label store cards, meaning they only work at the specific retailer (or sometimes its affiliated brands). They cannot be used at other stores, online retailers, or for other purchases.

What happens if I miss a payment on a jewelry store card?

Missing a payment doesn't just add a late fee — on deferred interest plans, it can also void your promotional financing, triggering the full retroactive interest charge from day one of your purchase. Always set up autopay for at least the minimum payment if you use one of these cards.

Is a jewelry store credit card worth it for an engagement ring?

Only if your credit score is below 660 and you can't qualify for a better card. If you have good credit, options like the Chase Freedom Unlimited (15-month true 0% APR) or Wells Fargo Reflect (up to 21 months) give you a longer, safer interest-free window — plus rewards. If you're financing a $4,000+ ring, using a card like Chase Sapphire Preferred can generate enough sign-up bonus points to cover flights for your honeymoon.

Bottom Line

Jewelry store credit cards serve a specific purpose: they give shoppers with fair credit access to promotional financing they might not get with a regular card. Among the available options, the Helzberg Diamonds Credit Card offers the most flexible promotional ladder, while the Crown Jewelers Card is the only option with no credit check requirement.

But for anyone with a credit score above 660, a general-purpose 0% APR card — particularly the Wells Fargo Reflect or Chase Freedom Unlimited — is a better deal in nearly every scenario. You get a longer, true 0% APR period with no deferred interest trap, plus rewards on your purchase.

Whatever you choose, understand deferred interest before you sign. The $0 annual fee and 12-month "no interest" offer only feels free until you read the fine print.

Ready to compare more cards? Browse our full credit card comparison tool to find the best option for your credit score and spending goals.

Disclaimer: Credit card terms change frequently. Always verify the current APR, fees, and promotional terms directly with the card issuer before applying. The information in this article is accurate as of April 2026.