Credit Card Comparison Tool: Find Your Best Card

Compare hundreds of credit cards side by side. Find the best rewards, lowest APR, or longest 0% intro offer matched to your actual spending habits.

The average American household carries 3.8 credit cards. Most of them aren't the right ones.

Not because people made bad choices — but because they compared cards the wrong way. They picked the biggest sign-up bonus or the lowest advertised APR without running the numbers against their actual life: what they spend, what they carry, and what they really want out of a card.

This guide gives you a full credit card comparison tool plus a framework for making the decision correctly. Use the tool to compare cards side by side. Read on to understand what actually matters — and what's mostly marketing noise.

Use the Credit Card Comparison Tool

Input your monthly spending by category, set your credit score range, and choose what you're optimizing for (rewards, low APR, balance transfer, or no annual fee). The tool ranks cards by estimated annual value to you — not a generic benchmark.

What Is a Credit Card Comparison Tool?

A credit card comparison tool lets you evaluate multiple cards side by side across the metrics that matter: APR, rewards structure, annual fees, sign-up bonuses, and any perks (lounge access, travel insurance, purchase protection).

The best tools go one step further: they let you plug in your spending habits and show you the estimated annual value of each card based on your numbers, not a hypothetical average user's.

That distinction matters more than most people realize. A card that earns 3% on dining is worth very different amounts to someone who spends $800/month at restaurants versus someone who barely eats out.

The 5 Things That Actually Matter When Comparing Cards

There are dozens of variables on any credit card offer page. Most of them are noise. These five are signal.

1. Your Net Annual Value

Net annual value = (rewards earned on your spending) + (sign-up bonus value) − (annual fee) ± (benefit value, if you'd actually use them).

This is the number the card comparison tool calculates for you. It's the only number that matters for rewards cards.

2. The APR (If You Ever Carry a Balance)

If you pay your balance in full every month, the APR is largely irrelevant — you'll never pay interest. If you sometimes carry a balance, even occasionally, the APR can easily wipe out any rewards you earn.

A card earning 2% cash back while charging 24% APR on a $1,000 balance for three months costs you roughly $60 in interest. That's more than the $20 in cash back you'd earn on that same $1,000 in spending.

Rule of thumb: If you carry a balance, prioritize the lowest APR. Rewards come second.

3. The Annual Fee Hurdle

An annual fee isn't inherently bad. A $95 card that earns you $340 in rewards is a better deal than a $0 card that earns you $180. What matters is whether you can clear the hurdle.

Use annual fee calculator to see exactly what spending level is required for a card's rewards to offset its fee.

4. The Sign-Up Bonus — But Valued Correctly

A "75,000 point" offer sounds impressive until you realize some programs value those points at 0.5 cents each (worth $375) and others at 2.0 cents each (worth $1,500).

Comparing raw point counts across different loyalty programs is meaningless. Always compare bonuses in estimated dollar value. Our comparison tool does this automatically using per-program points valuations.

5. Your Credit Score Eligibility

The best card in the world won't help you if you don't qualify for it. Applying for cards outside your credit range wastes a hard inquiry and can temporarily ding your score.

Filter cards by your credit score band before you start comparing.

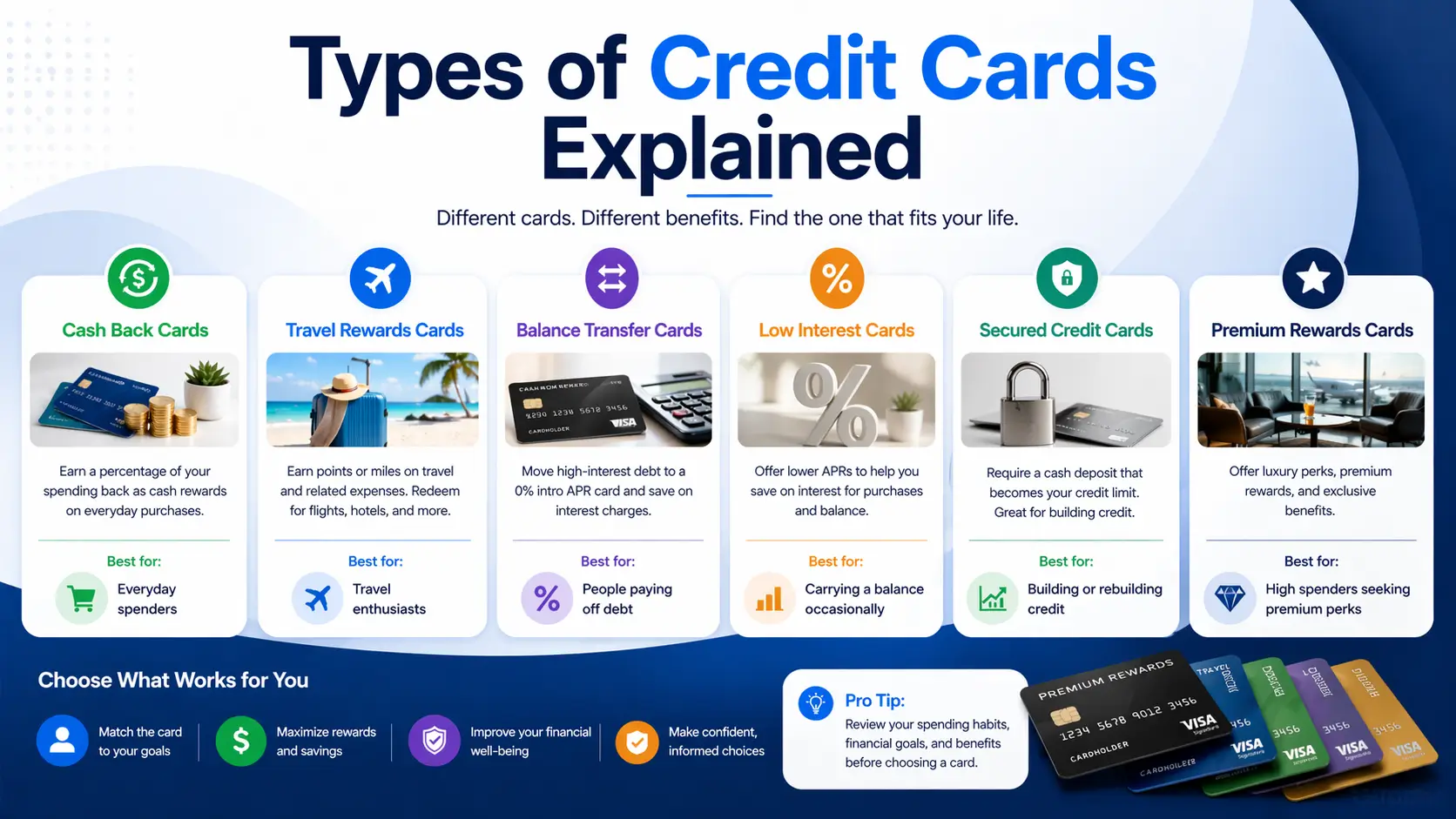

Types of Credit Cards Explained

Not every card is built for the same purpose. Comparing a travel rewards card against a balance transfer card is like comparing a hiking boot to a running shoe.

Cash Back Cards

Earn a percentage of every purchase back as statement credit or deposited to your bank account. Best for people who want simplicity — no points programs to navigate, no transfer partners to learn.

Best if: You want straightforward value with no complexity.

Travel Rewards Cards

Earn points or miles redeemable for flights, hotels, and transfers to airline/hotel programs. Highest potential value per dollar spent — but only if you understand how to redeem well.

Best if: You travel regularly and are willing to optimize redemptions.

Balance Transfer Cards

Offer a 0% introductory APR on balances transferred from other cards, typically for 12–21 months. Designed for debt payoff, not spending rewards.

Best if: You're carrying high-interest credit card debt and have a plan to pay it down.

Low APR / 0% Intro Purchase Cards

Similar to balance transfer cards but the 0% period applies to new purchases. Useful for planned large expenses.

Best if: You're about to make a major purchase and want to spread payments interest-free.

Secured Cards

Require a security deposit that becomes your credit limit. Designed for building or rebuilding credit.

Best if: You have limited or damaged credit history.

Student Cards

Designed for college students with limited credit history. Lower limits, simpler rewards, often no annual fee.

Best if: You're a student establishing credit for the first time.

Business Cards

Earn rewards on business spending categories (office supplies, advertising, travel). Keep business and personal expenses separate.

Best if: You have business expenses to put on a card.

How to Compare Credit Cards Step by Step

Here's the process to use alongside the comparison tool.

Step 1: Identify your primary goal. Are you trying to earn rewards, pay down debt, build credit, or finance a large purchase? Your goal determines which card type to focus on. Don't mix categories — a traveler rewards card and a 0% APR debt-payoff card serve fundamentally different purposes.

Step 2: Know your credit score range. Pull your score from your bank app, Credit Karma, or any free source before you start. Filter the comparison tool to cards within your range. This narrows the field to cards you can actually get.

Step 3: Enter your real monthly spending. Be honest. Look at last month's bank statement and break down spending by category: groceries, dining, gas, travel, subscriptions, everything else. Most people underestimate their dining spend and overestimate their travel spend.

Step 4: Sort by net annual value. Let the tool rank cards by what they'd actually pay you given your spending. Ignore the raw rewards rates — what matters is how those rates apply to your specific mix.

Step 5: Check the annual fee math. For any card with an annual fee, verify: does the projected annual value exceed the fee by enough to justify the effort? A card that earns you $50 more than a free card but requires you to activate quarterly categories and track rotating bonuses may not be worth it for you.

Step 6: Verify eligibility and apply. Once you've picked your top one or two options, verify you meet the credit score requirement and check for any application restrictions (e.g., Chase 5/24 rule, American Express "once per lifetime" bonus rules).

How to Use a Rewards Estimator

Our rewards estimator works by applying each card's category-specific earn rates to your monthly spending breakdown, then annualizing the result and subtracting the annual fee.

Here's a quick example:

Hypothetical spending profile: $800 dining, $400 groceries, $200 gas, $600 other

Card A (3% dining, 1% everything else, $0 annual fee): ($800 × 3%) + ($1,200 × 1%) × 12 = $288 + $144 = $432/year

Card B (2% on everything, $0 annual fee): ($2,000 × 2%) × 12 = $480/year

Card B wins for this profile, even though Card A has a higher headline dining rate.

This is why a personalized estimator beats generic "best card" lists. The answer depends entirely on your numbers.

Run your spending profile in the comparison tool →

Common Mistakes When Comparing Credit Cards

Comparing rewards rates without accounting for annual fees. A 3% card with a $550 fee often loses to a 2% card with no fee unless you spend heavily in bonus categories.

Taking the sign-up bonus at face value. Always convert to dollar value using the program's estimated cents-per-point. "100,000 points" ranges from $500 to $2,000 depending on the program.

Ignoring redemption complexity. Points are only as good as your ability to redeem them at good value. If you won't navigate transfer partners, a cash-back card will serve you better than a travel card with theoretically higher value.

Applying for multiple cards at once. Each application is a hard inquiry. Multiple inquiries in a short window lower your credit score. Apply for your top choice, wait for the result, then decide whether to apply for a backup.

Optimizing for the wrong thing. If you carry a balance, optimizing for rewards while ignoring APR is like rearranging deck chairs. Prioritize the APR until the balance is gone.

Best Credit Cards by Category

Note: Card offers change frequently. Use the comparison tool for current rates and sign-up bonus availability.

Best for Flat-Rate Cash Back

A card earning a simple, flat 2% on everything is often the highest-value card for people with varied spending who don't want to manage categories. Look for no annual fee versions for maximum net value.

Best for Dining and Entertainment

Dining-focused earners can pull 4–5x points per dollar at restaurants with the right card. If you spend $600+ per month on dining, a premium dining card typically clears its annual fee with room to spare.

Best for Groceries

The grocery category is one of the most competitive earn rates available. Look for cards earning 4–6% at U.S. supermarkets, and check whether warehouse stores (Costco, Sam's Club) qualify — many don't.

Best for Balance Transfers

Evaluate balance transfer cards on: (1) length of the 0% intro APR period, (2) the balance transfer fee (typically 3–5%), and (3) what the APR becomes after the intro period. Balance transfer calculator shows total cost at your balance size across different transfer terms.

Best for Travel Rewards

Travel rewards cards earn the most per dollar on travel and dining, offer transfer partners that can unlock premium cabin redemptions, and typically include perks (lounge access, travel insurance, Global Entry credit) that offset the annual fee.

Evaluate travel cards by: (1) estimated points value at your redemption style, (2) whether the annual perks offset the fee, and (3) how practical the transfer partners are for your travel patterns.

Frequently Asked Questions (FAQs)

What's the best credit card right now?

There's no universal answer — it depends on your spending mix, credit score, and what you're optimizing for. Use the comparison tool with your real spending data to find your best card.

How many credit cards should I have?

Most people benefit from 1–3 cards: one everyday earner, potentially one for a specific high-spend category, and one for travel if you travel regularly. More than that and the management overhead often outweighs the marginal rewards.

Does applying for a credit card hurt my credit score?

Yes, briefly. A hard inquiry typically drops your score by 2–5 points and remains on your report for two years. The impact diminishes after a few months and disappears from scoring models after a year.

How often should I reassess my credit cards?

Once a year is a reasonable cadence. Review whether your spending patterns have changed significantly, whether better offers have entered the market, and whether your annual fee cards are still earning their keep.

Is a card with an annual fee worth it?

Only if the rewards and benefits you'd actually use exceed the fee. Use our annual fee calculator to check. If the card earns you $250/year in rewards but costs $95, the math works. If you're paying $550 for perks you never use, it doesn't.

What credit score do I need for a good rewards card?

Most premium rewards cards require good to excellent credit (typically 690+). Some strong mid-tier rewards cards are available starting around 670. Use the credit score filter in the comparison tool to see what you qualify for.

Can I get a credit card with no credit history?

Yes — secured cards and some student cards are designed for this. They typically have lower limits and simpler rewards structures, but they're the right first step for building credit history.

Compare credit cards now — free, no sign-up required →